Set up your transaction tracking

Before calculating capital gains, you need a complete picture of your crypto activity. The IRS treats virtual currency as property, meaning every trade, swap, or transfer can trigger a taxable event. If your data is scattered across five different exchanges and a hardware wallet, you are likely missing information that could lead to an underreported income notice.

Think of your transaction history like a bank statement. You wouldn’t try to reconcile your checking account using three different spreadsheets and a handful of printed receipts. You need one consolidated view. Aggregating your data now prevents the "I forgot to export from that one DEX" panic during tax season.

Here is the sequence to build that single source of truth.

Log into each exchange where you have traded (Coinbase, Binance, Kraken, etc.). Navigate to the tax or transaction history section and download your full trade history in CSV format. Ensure you include all dates, prices, and fees. Schwab notes that virtual currencies can result in real tax liabilities, so accuracy here is non-negotiable.

For non-custodial wallets (MetaMask, Ledger, Trezor), use blockchain explorers or wallet-specific export tools to generate a list of all incoming and outgoing transactions. This includes gas fees paid, which are often overlooked but are part of your cost basis.

Upload your CSVs into a crypto tax platform like Koinly, CoinTracker, or TokenTax. These tools map the transactions to the correct tax forms and automatically calculate your gains and losses based on the accounting method you choose (FIFO, LIFO, or Specific ID).

Review the imported transactions for duplicates or missing entries. Cross-reference your total crypto balance in the software against your actual holdings. If the numbers don’t match, dig into the individual transactions to find the error before filing.

Getting this foundation right saves hours of manual calculation later. Once your data is aggregated and verified, you can move on to identifying specific taxable events.

Identify taxable events in your flow

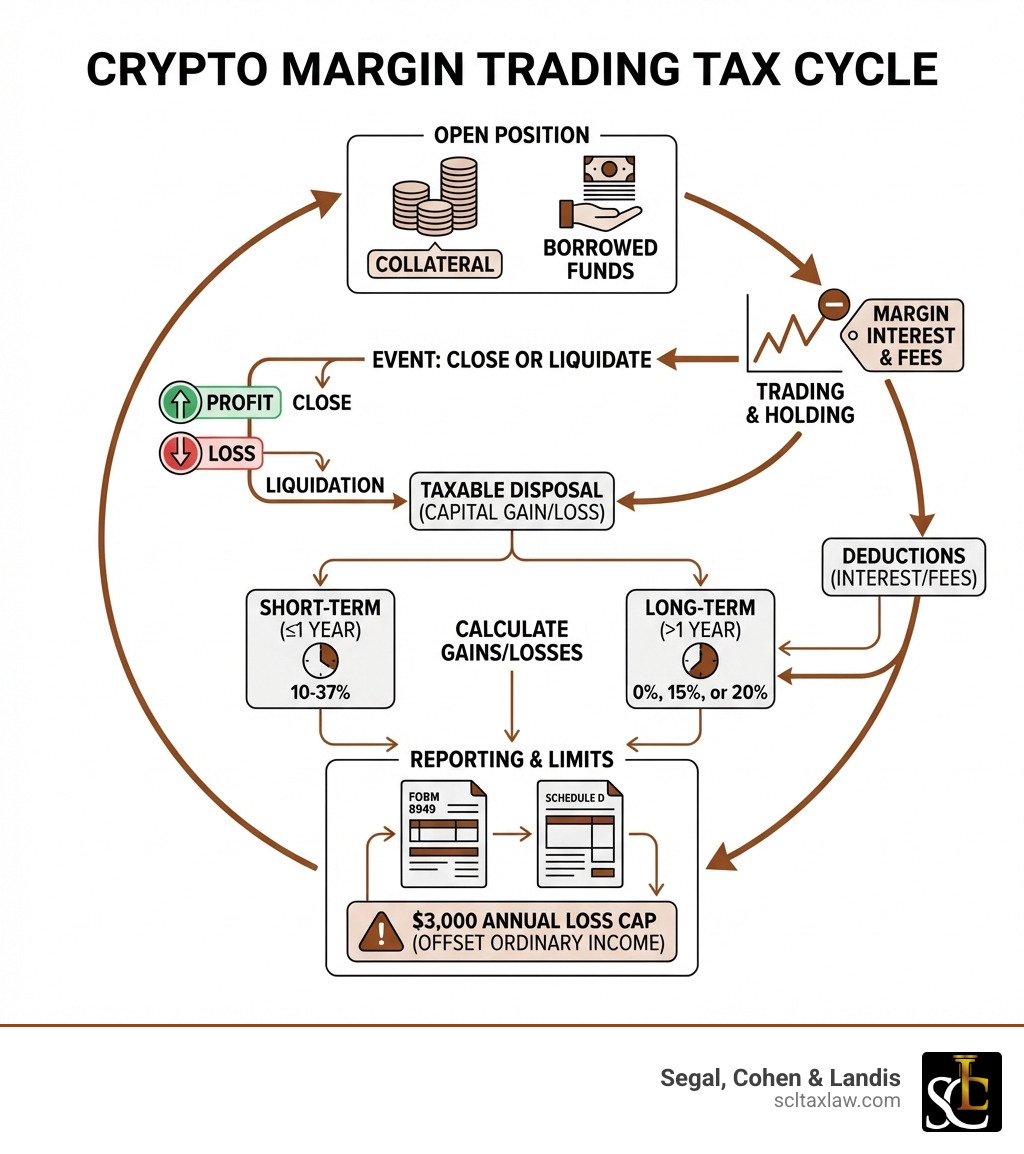

Active trading creates a high volume of transactions. The IRS treats cryptocurrency as property, not currency. This classification means that almost every interaction with your crypto assets triggers a tax calculation. You need to separate transactions that change your tax liability from those that do not. Misidentifying these events leads to either over-reporting or under-reporting.

Sales and swaps

Selling crypto for fiat currency (like USD) is a taxable event. You must calculate the gain or loss based on the difference between your cost basis and the sale price. Swapping one cryptocurrency for another, such as trading Bitcoin for Ethereum, is also taxable. The IRS views this as disposing of one asset to acquire another. Even if you do not receive fiat, the transaction triggers a capital gain or loss.

Staking and mining rewards

Income from staking, mining, or airdrops is taxable as ordinary income. The value of the crypto at the time you receive it becomes your cost basis. This applies whether the reward is deposited into a exchange wallet or a self-custody wallet. You report this income on your tax return in the year you receive it. Subsequent sales of these rewards will then trigger capital gains or losses based on that initial basis.

Non-taxable transfers

Moving crypto between your own wallets is not a taxable event. Sending Bitcoin from your hardware wallet to your exchange wallet does not trigger a gain or loss. You have not disposed of the asset; you have merely changed its location. However, you must track the cost basis through these transfers. If you send crypto to someone else, or use it to pay for goods or services, that is a taxable disposal.

Gift and inheritance rules

Receiving crypto as a gift is generally not taxable for the recipient. The giver may have gift tax implications if the value exceeds the annual exclusion limit. Inheriting crypto is also typically not a taxable event for the beneficiary. However, the cost basis may be stepped up to the fair market value at the time of death, which can significantly reduce future capital gains tax. Always consult a tax professional for estate planning involving crypto assets.

Choose the right reporting software

Active traders generate thousands of transactions, making manual calculation impossible. You need a crypto tax tool that automates the heavy lifting: syncing with your exchanges, classifying taxable events, and generating the specific IRS forms you need. The right software acts as your bridge between messy on-chain data and compliant tax filings.

Start by verifying that the platform supports every chain you trade on. If you use Solana or Polygon, a tool that only handles Ethereum and Bitcoin will leave gaps in your reporting. You also need to check for broker integration. The best tools pull data directly from your centralized exchanges (CEX) to pre-fill Form 8949, reducing the risk of human error during the import process.

| Software | Volume Handling | Chain Support | IRS Form Gen |

|---|---|---|---|

| Koinly | High | 200+ | Form 8949 |

| CoinTracker | High | 100+ | Form 8949 |

| TokenTax | Very High | 100+ | Form 8949 |

| TradeLog | Enterprise | Limited | Schedule D |

For high-frequency traders, specialized software like TradeLog is often preferred because it treats your crypto activity as a business, allowing for Section 475(f) mark-to-market accounting. For most active traders, Koinly or CoinTracker offer the best balance of automation and cost. Look for platforms that offer real-time syncing, so your data is always up to date without manual CSV uploads.

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY654_QL65_.jpg)

As an Amazon Associate, we may earn from qualifying purchases.

Before committing, test the free trial. Import a small sample of your transaction history and see how the software categorizes your trades. If it misclassifies staking rewards or airdrops, the final tax bill will be wrong. Choose a tool that gets the basics right before you scale up to your full portfolio.

Apply tax-loss harvesting strategies

Tax-loss harvesting is one of the most effective ways for active traders to reduce their crypto tax liability. The strategy involves selling assets that have decreased in value to realize a loss, which can then be used to offset capital gains from other trades. If your losses exceed your gains, you can use the remaining loss to reduce your ordinary income, up to a specific annual limit.

Here is how to execute this strategy while staying compliant with IRS regulations:

Review your portfolio to find cryptocurrencies that have dropped in value since you purchased them. Only assets with a negative unrealized gain are candidates for this strategy. You can use tax software to generate a list of these positions automatically.

Sell the identified assets to realize the loss. Ensure the transaction is recorded accurately in your tax tracking software. The loss is realized only when the trade is completed and settled.

Use the realized loss to offset any capital gains you have realized during the tax year. If your losses exceed your gains, you can deduct up to $3,000 of the remaining loss against your ordinary income (such as wages or salary). Any unused loss carries forward to future tax years.

Be careful not to buy the same or a "substantially identical" cryptocurrency within 30 days before or after the sale. While the IRS has not explicitly confirmed that the wash-sale rule applies to crypto, many tax professionals advise following it anyway to avoid disputes. Wait at least 31 days before repurchasing the same asset.

This approach requires meticulous record-keeping. Using specialized tax software can help you track these transactions and identify harvesting opportunities automatically, ensuring you stay compliant while minimizing your tax bill.

Review and file your returns

Before you hit submit, treat your crypto tax return like a financial audit. Active traders generate massive amounts of data, and a single misclassified transaction can trigger IRS notices or incorrect capital gains calculations. This final review ensures your Schedule 1 and Schedule D forms accurately reflect your activity.

Every crypto sale, trade, or exchange must be reported on Form 8949. Check that each transaction includes the date acquired, date sold, proceeds, cost basis, and gain or loss. Ensure you’ve selected the correct box (Box A, B, or C) to indicate whether basis was reported to the IRS. Missing or mismatched data here is the most common source of filing errors.

Schedule D summarizes the data from your Form 8949 entries. Verify that the totals on Schedule D match the subtotals from Form 8949 exactly. If you have net capital losses, confirm that the deduction limit ($3,000 for single filers) is applied correctly. Any discrepancy between these two forms will cause processing delays or automated adjustments.

Compare your internal records against the 1099-B forms provided by exchanges like Coinbase, Kraken, or Binance. Look for transactions that appear on the 1099-B but are missing from your tax software, or vice versa. Unreported transactions are a frequent trigger for IRS correspondence, so ensure every taxable event is accounted for.

While you don’t submit transaction logs with your return, keep detailed records of all trades, wallet addresses, and timestamps. If you used a third-party tax software, export the final report and save it as a PDF. These records serve as your proof of cost basis and transaction history if the IRS questions your filing.

-

All Form 8949 entries match exchange 1099-B reports

-

Schedule D totals reconcile with Form 8949 subtotals

-

Cost basis method (FIFO, LIFO, or Specific ID) is consistently applied

-

State tax forms are prepared if required by your residency

-

Tax software generated a final review report with no errors

Once you’ve completed this checklist, you’re ready to file. Use the IRS Free File program if your income is below the threshold, or submit electronically through a certified tax preparer. Accurate filing now prevents costly corrections later.

Common crypto tax: what to check next

Active traders often face complex tax scenarios that go beyond simple buy-and-hold strategies. Understanding these rules is essential for staying compliant without overpaying.

How are short-term vs. long-term crypto gains taxed?

The holding period determines your tax rate. If you sell crypto after holding it for more than one year, you pay long-term capital gains rates, which range from 0% to 20% depending on your income. If you sell within a year, those gains are taxed as ordinary income, ranging from 10% to 37%.

Do I need to report crypto if I didn’t cash out?

Yes. Swapping one cryptocurrency for another, using crypto to pay for goods, or receiving crypto as payment is a taxable event. You must report the fair market value of the asset at the time of the transaction. Not cashing out into fiat currency does not exempt you from reporting requirements.

What are the best resources for crypto tax education?

For traders seeking structured learning, platforms like AvaAcademy offer free online courses covering cryptocurrency trading basics. Additionally, consulting the IRS guidance on virtual currency and using certified tax software can help ensure accurate reporting of complex trading activities.

No comments yet. Be the first to share your thoughts!