Get crypto tax education active right

Before you file or rebalance, you need a working knowledge of how the IRS treats your specific transactions. The agency classifies crypto as property, which means every swap, trade, or transfer triggers a taxable event. Without understanding these basics, you risk misreporting gains or missing new reporting requirements under the Infrastructure Investment and Jobs Act.

Start by reviewing official guidance from trusted financial institutions. Fidelity and Intuit ProConnect offer clear breakdowns of how crypto taxes work, including how to report sales and calculate cost basis. These resources help you distinguish between ordinary income and capital gains, which is essential for accurate filing.

If you are new to this, consider structured learning. Platforms like AvaAcademy provide free online courses that cover trading mechanics and tax implications. These courses help you understand the difference between short-term and long-term holdings, which directly impacts your tax rate. Holding crypto for more than a year can qualify you for lower capital gains rates, while shorter holds are taxed as ordinary income.

Once you grasp the fundamentals, move to practical application. Use this knowledge to review your transaction history and identify any reporting gaps. This preparation ensures you are ready to handle the new infrastructure rules and avoid penalties.

Work through the steps

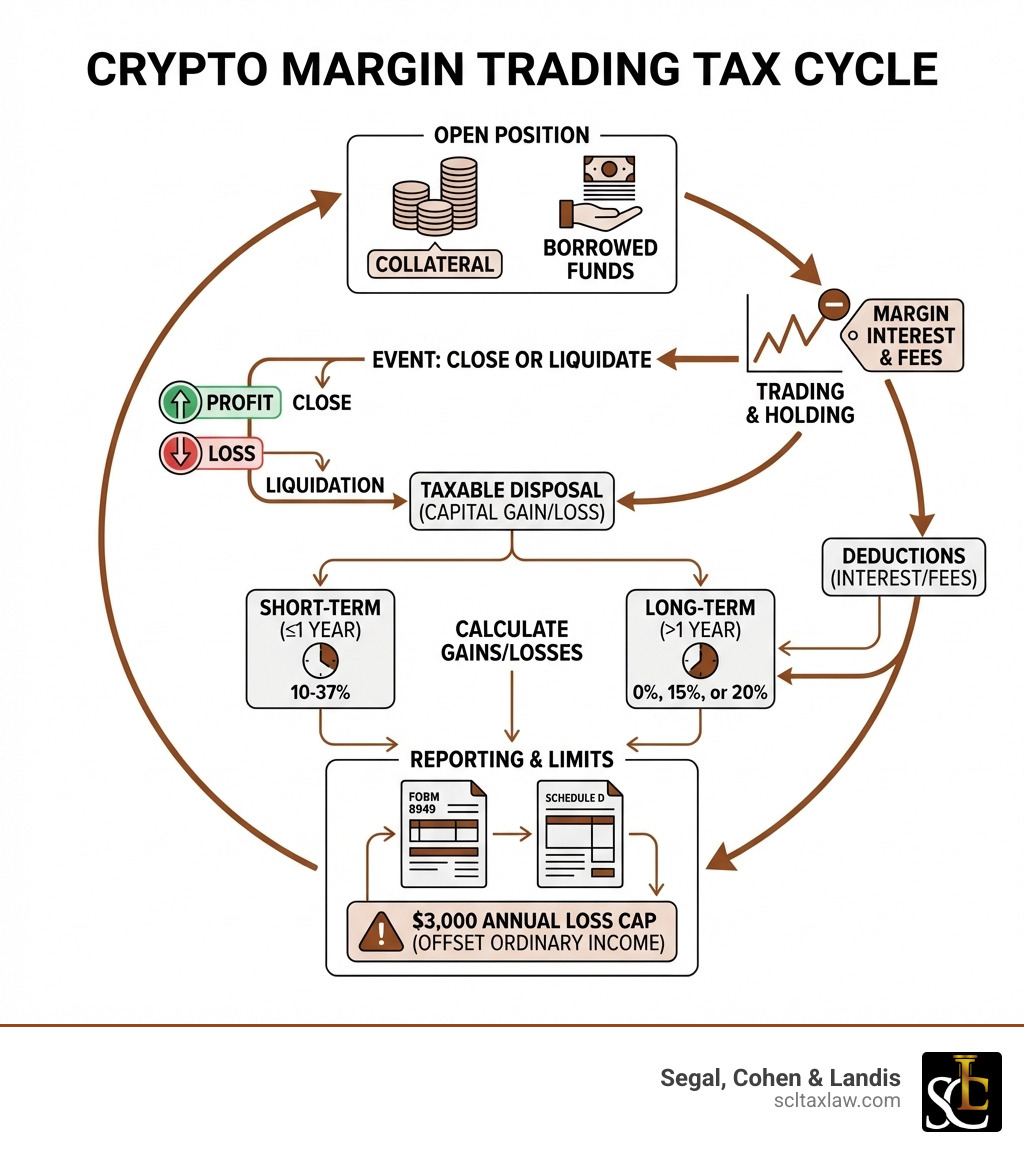

Active traders face a heavier compliance burden than long-term holders. The IRS treats cryptocurrency as property, meaning every swap, trade, or transfer triggers a taxable event. Recent infrastructure rules under the Inflation Reduction Act have tightened reporting requirements for exchanges, making accurate record-keeping non-negotiable.

Follow this sequence to structure your tax workflow before filing season. This approach minimizes errors and ensures you capture all allowable deductions.

Export CSV files from every exchange, wallet, and decentralized protocol you used. Include spot trades, staking rewards, airdrops, and NFT sales. Do not rely on a single platform’s summary; discrepancies between sources are common and can trigger audits. Use a tax software that supports bulk imports to merge these datasets into a single ledger.

Not all crypto movements are taxable. Separate disposals (sales, swaps, spending) from non-taxable events (transfers between your own wallets, staking rewards which are ordinary income, or hard forks). Misclassifying a transfer as a sale creates a phantom tax liability. Tag each row in your ledger with its specific event type to ensure accurate cost-basis calculation.

Choose a consistent accounting method. First-In, First-Out (FIFO) assumes the oldest coins are sold first, which often results in higher short-term capital gains if prices have risen. Specific Identification allows you to pick exactly which coins you sold, offering more control over your tax bill. You must document your chosen method and stick to it across all transactions to avoid IRS rejection.

Offset gains with losses using tax-loss harvesting. If you sold an asset at a loss, you can deduct up to $3,000 against ordinary income annually, carrying forward any excess. Be mindful of the wash-sale rule, which currently does not apply to crypto but may change. Keep detailed records of these sales to prove the losses were genuine and not part of a repurchase scheme within 30 days.

New infrastructure rules require exchanges to issue Form 1099-DA starting in 2025. Compare these forms against your internal ledger. Discrepancies in cost basis or missing transactions are frequent. If an exchange reports a sale you don’t recognize, or omits a loss, contact the platform immediately. Do not file using incomplete data from the exchange alone.

-

Exported CSVs from all exchanges and wallets

-

Classified transactions into taxable and non-taxable events

-

Selected and documented FIFO or Specific ID method

-

Calculated total gains and losses

-

Harvested losses to offset gains

-

Reconciled internal ledger with Form 1099-DA

Fix common mistakes

Most active traders lose money to the IRS not because they trade too much, but because they ignore how crypto is classified. The IRS treats digital assets as property, not currency. This distinction changes everything about how you report gains, losses, and even staking rewards. When you mix up these categories, you risk audits, penalties, or paying more tax than necessary.

Here are the most frequent errors and how to correct them before filing.

Ignoring the holding period

Many traders assume all profits are taxed the same way. They are not. If you hold crypto for a year or less, gains are treated as ordinary income, taxed at your standard federal rate of 10% to 37%. If you hold for more than a year, you qualify for long-term capital gains rates of 0%, 15%, or 20%.

The Fix: Track your acquisition date for every asset. If you are close to the one-year mark and facing a large gain, consider holding. The tax savings can be significant, but weigh this against market risk. Never hold a losing asset just for the tax break; cut losses early.

Mixing up swaps and sales

You might think that swapping Bitcoin for Ethereum on a decentralized exchange isn’t a taxable event because you didn’t receive fiat currency. It is. Any exchange of one crypto for another is a taxable disposition. You must calculate the fair market value of the asset you received at the time of the swap and compare it to your cost basis.

The Fix: Use tax software that integrates with major wallets and exchanges. Manual tracking of thousands of swaps is prone to error. Ensure your software captures the exact timestamp and USD value at the moment of the swap.

Overlooking staking and airdrops

Income from staking, yield farming, or airdrops is taxable as ordinary income at the fair market value on the day you received them. Many traders forget to report these "free" assets. When you eventually sell that staked crypto, your cost basis is the value you reported as income. If you ignore the initial income, you might underreport your basis later, leading to higher taxes or an audit.

The Fix: Record the USD value of every airdrop or staking reward on the day it hits your wallet. This becomes your cost basis. When you sell, subtract this basis from the sale price to determine your gain or loss.

Failing to reconcile 1099 forms

Exchanges are required to send Form 1099-MISC or 1099-K for certain activities. However, these forms often contain errors or miss off-exchange transactions. If you only report what is on the 1099, you might be underreporting. Conversely, if you report everything twice, you overpay.

The Fix: Treat the 1099 as a starting point, not the final answer. Reconcile every transaction from your wallet history against the exchange’s report. If the exchange missed a transaction, you are still responsible for reporting it. If the 1099 includes transactions you didn’t have, you must file an amended return or provide documentation to the IRS.

By avoiding these common mistakes, you can stay compliant and keep more of your trading profits. Always consult a tax professional for your specific situation.

Crypto tax education for active traders: what to check next

Active traders face unique tax complexities that general guides often miss. The 2026 infrastructure rules tighten reporting requirements, making precise record-keeping essential. Below are answers to the most frequent questions from traders navigating these changes.

No comments yet. Be the first to share your thoughts!