Crypto tax education for active traders: infrastructure first

High-frequency crypto trading creates a reporting burden that standard tax software rarely handles well. The IRS now receives direct transaction data via Form 1099-DA, meaning every US-based exchange reports your gross proceeds. You cannot hide activity; you can only manage the complexity.

Education here means understanding how your specific trading style interacts with tax rules. It is not about generic advice. It is about knowing how wash sales, cost basis methods, and short-term capital gains apply to your volume. Without this infrastructure, you risk overpaying or facing audits.

The 1% rule and capital preservation

The 1% rule is a risk management strategy, not a tax deduction. It dictates that you never risk more than 1% of your total account equity on a single trade. For active traders, this preserves capital during volatile markets. While it does not directly lower your tax bill, it prevents the catastrophic losses that complicate tax loss harvesting strategies. Stable capital allows for consistent, reportable gains rather than chaotic, unmanageable drawdowns.

The 30-day rule and wash sales

The 30-day rule applies when you sell a cryptocurrency and buy the same asset within 30 days. The cost basis of the new purchase is adjusted against the proceeds of the sold asset. This prevents traders from claiming artificial losses by immediately repurchasing the same token. Active traders must track these repurchases closely to ensure their cost basis calculations remain accurate and compliant with IRS guidelines.

Avoiding capital gains tax legally

You can legally avoid paying capital gains tax on crypto by holding assets longer than one year, converting them to long-term capital gains rates. Alternatively, you can transfer crypto between your own personal wallets, which is not a taxable event. Gifting cryptocurrencies to family members or charitable organizations is another valid strategy. However, simply buying and holding without selling is the only way to defer taxes entirely until disposal.

How the IRS tracks your sales

The IRS knows you sold cryptocurrency because exchanges are required to collect KYC information and report activity. Starting with the 2025 tax year, this reporting happens via Form 1099-DA. This form details gross proceeds from digital asset transactions. If your records do not match the 1099-DA, you will receive notices. Reconciling these forms is the first step in any active trader's tax strategy.

Crypto tax education active choices that change the plan

Use this section to make the Active Trader Tax Strategy decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

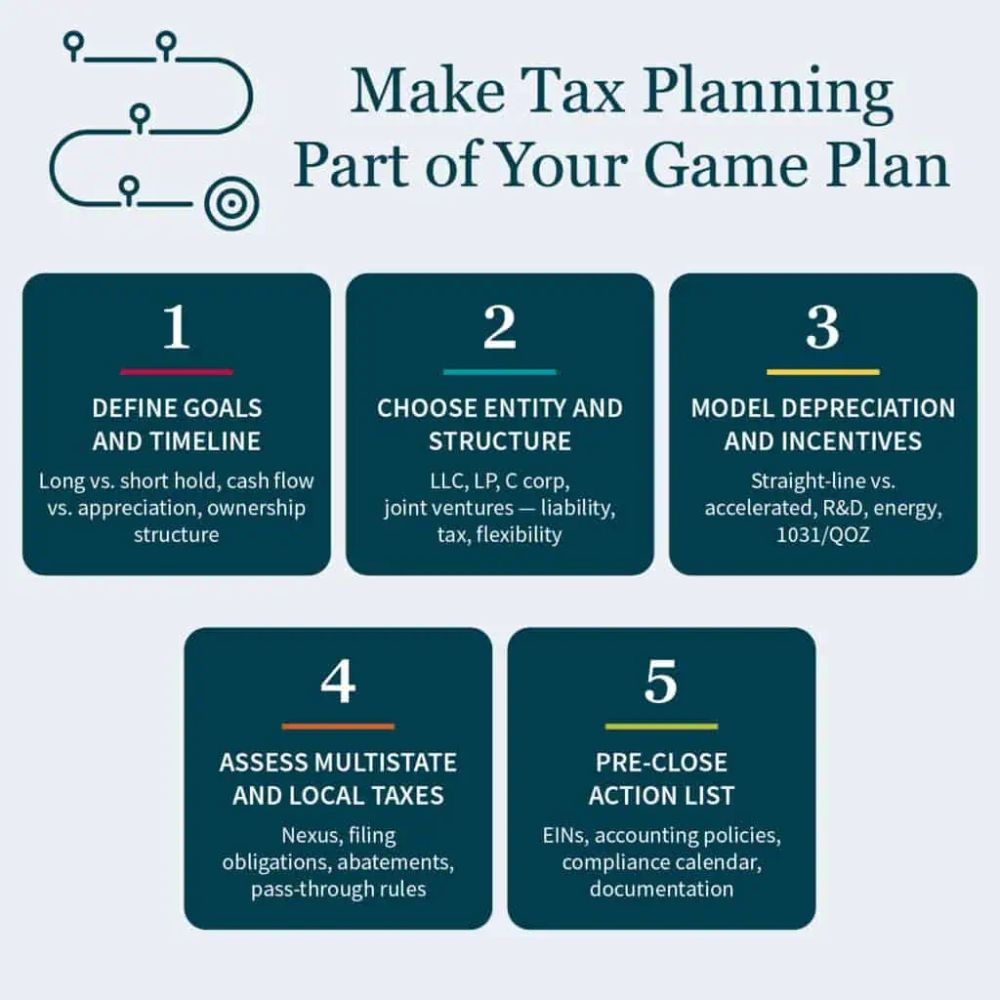

Build Your 2026 Crypto Tax Decision Framework

High-frequency crypto trading generates noise. Without a clear decision framework, you will miss deductions, misreport cost basis, or trigger audits. The IRS now tracks digital asset transactions directly through Form 1099-DA, making manual guesswork obsolete.

Use these five steps to structure your tax strategy for the 2026 filing season. Each step addresses a specific compliance or optimization risk.

Most active traders default to First-In, First-Out (FIFO). However, for high-frequency crypto traders, Specific Identification often yields lower capital gains by allowing you to match high-cost purchases against recent sales. Verify that your trading software supports this method before the tax year closes.

Keep active trading wallets separate from long-term holdings. This prevents commingling of assets, which complicates cost basis calculations. If you sell a crypto asset and buy the same one back within 30 days, the wash sale rule may apply depending on current IRS guidance, affecting your loss deductions.

Exchanges provide gross proceeds, but not your adjusted cost basis. Use a dedicated tax tool to import API data from every exchange and wallet. This ensures you capture every swap, stake reward, and airdrop. Missing even one transaction can trigger an IRS notice when their Form 1099-DA data is matched against your return.

If you trade full-time, you may qualify for Mark-to-Market (MTM) accounting under Section 475(f). This status allows you to deduct trading losses as ordinary business expenses, bypassing the $3,000 capital loss deduction limit. However, you must elect this status by the tax deadline of the prior year.

General CPAs often lack expertise in crypto-specific nuances like DeFi interactions or NFT trading. Hire a specialist who understands the 2026 regulatory landscape. They can help you navigate complex scenarios like staking rewards, lending income, and cross-chain bridges.

By following this framework, you transform tax compliance from a reactive burden into a strategic advantage. Start preparing your records now to avoid end-of-year chaos.

Spotting the Weak Options in Crypto Tax Strategy

High-frequency crypto traders often chase complex deductions or aggressive interpretations of tax law, only to find themselves facing audits for unsupported claims. The IRS has significantly tightened its reporting requirements, making it essential to distinguish between legitimate planning and risky missteps. Before committing to a strategy, verify that your approach aligns with current official guidance rather than outdated blog posts or unverified social media tips.

The 30-Day Rule Misconception

Many traders confuse the IRS wash sale rule with a simple "30-day rule." While the wash sale rule currently does not apply to crypto, some states or specific interpretations might suggest otherwise, or traders might mistakenly believe that selling and rebuying within 30 days avoids tax. In reality, any sale triggers a taxable event. If you sell at a loss and repurchase within 30 days, you do not get the wash sale deduction for federal purposes, but you must still report the gain or loss accurately. Relying on this "rule" to hide losses is a common mistake that leads to underreported income.

The 1% Rule: Risk vs. Tax

The "1% rule" is primarily a risk management strategy, not a tax strategy. It dictates that you never risk more than 1% of your account equity on a single trade. While this protects your capital, it does not reduce your tax liability. Traders often mistakenly believe that limiting risk limits taxable gains. In fact, frequent small wins and losses still require detailed record-keeping. If you are active trading, the volume of transactions may qualify you for trader tax status, but the 1% rule itself offers no tax advantage. Focus on accurate cost basis tracking instead.

Avoiding Capital Gains: Don't Sell

The most effective way to avoid capital gains tax is to not sell. If you hold your crypto, you defer taxes indefinitely. Transferring between personal wallets or gifting crypto (within annual exclusion limits) also avoids immediate tax events. However, this is not a strategy for active traders who need liquidity. If you must sell, ensure you are using the correct cost basis method (FIFO or Specific Identification) to minimize gains. Do not rely on vague advice to "hold forever" if your strategy requires active management.

How the IRS Knows

The IRS knows about your sales because US-based exchanges are now required to report digital asset transactions via Form 1099-DA. This means your gross proceeds and cost basis are directly shared with the IRS. Attempting to hide transactions through decentralized exchanges or peer-to-peer trades is increasingly risky and easily traced through blockchain analytics. Ensure your tax software reconciles your exchange reports with your internal records to avoid discrepancies that trigger audits.

Crypto tax education for active traders strategy: what to check next

Active traders face unique tax complexities that standard guides often miss. Understanding these specific rules helps you structure your trades to minimize liability while staying compliant. Here are the most common questions active traders ask about crypto taxation.

What is the 1% rule in crypto?

The 1% rule is a risk management strategy, not a tax law, but it directly impacts your tax outcomes by preserving capital. It dictates that you never risk more than 1% of your total account equity on a single trade. By limiting downside exposure, you prevent catastrophic losses that are difficult to recover from tax-wise, ensuring your portfolio remains viable for future profitable trades.

What is the 30 day rule in crypto?

The 30-day rule is the UK’s equivalent of the US wash sale rule. If you sell a cryptocurrency at a loss and buy the same asset back within 30 days, the loss is disallowed for tax purposes. Instead, the loss is added to the cost basis of the new holdings. This prevents traders from claiming artificial losses to reduce their tax bill while maintaining their market position.

How do I avoid paying capital gains tax on crypto?

You can legally reduce or defer capital gains tax by holding assets for over a year to qualify for long-term rates, which are typically lower than short-term ordinary income rates. Additionally, you can offset gains with losses from other trades (tax-loss harvesting). Transferring crypto between your own wallets does not trigger a taxable event, nor does gifting crypto to family in many jurisdictions, provided you do not sell the asset first.

How does the IRS know if you sell cryptocurrency?

The IRS tracks crypto sales primarily through direct reporting from US-based exchanges. Starting with the 2025 tax year, platforms must report gross proceeds using Form 1099-DA. These forms are generated using Know Your Customer (KYC) data, linking your digital asset transactions directly to your identity. Even non-US exchanges may share data through international treaties, making complete anonymity difficult for active traders.

No comments yet. Be the first to share your thoughts!