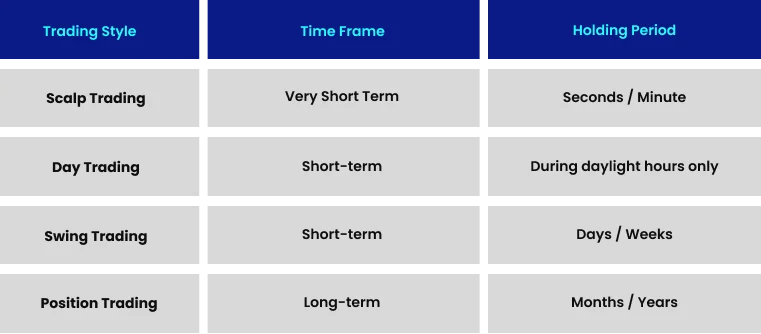

Determine your trader status

Before you file, you need to know how the IRS views your activity. This isn't just a semantic distinction; it dictates your entire tax strategy. The difference between an investor and an active trader changes how you report gains, deduct losses, and handle inventory.

Most crypto participants are classified as investors. If you buy and hold, or trade occasionally, you are likely an investor. Your profits and losses are treated as capital gains or losses. You report these on Schedule D and Form 8949. The tax rates depend on how long you held the asset: short-term rates apply to assets held less than a year, while long-term rates apply to those held longer. Fidelity outlines these basics clearly for those new to the space.

If you trade frequently, with high volume and regularity, you might qualify as a trader in securities. This is a specific IRS classification that requires meeting strict criteria. You must be seeking to profit from daily market movements, not just long-term appreciation. The IRS looks at factors like the frequency of trades, holding period, and the extent of your trading activity. If you meet this threshold, you can elect mark-to-market accounting under Section 475(f).

The mark-to-market election allows you to treat all crypto positions as sold at the end of the tax year. This means you report unrealized gains and losses as if you sold everything. The benefit? You can deduct trading losses against ordinary income, up to $3,000 for investors, but potentially fully for traders. There is no wash sale rule for traders, which can be a major advantage. However, this also means you lose the benefit of long-term capital gains rates.

Misclassifying yourself can lead to severe penalties. If the IRS determines you are an investor but you claimed trader status, you could face back taxes and interest. Conversely, if you are a trader but don't elect mark-to-market, you might miss out on significant deductions. E-Trade provides additional context on how different crypto types are taxed, which is useful for understanding the broader landscape.

To determine your status, track your trading activity. Count the number of trades, the holding periods, and the sources of your income. If you are spending most of your waking hours analyzing markets and executing trades, you may have a strong case for trader status. Consult a tax professional who specializes in crypto to make the final determination. This decision impacts your taxes for years to come, so get it right.

Track every transaction accurately

Manual spreadsheets collapse under the weight of high-frequency trading. If you execute more than a few trades a week, or interact with decentralized exchanges, your transaction history likely contains hundreds or thousands of entries. The IRS treats each crypto-to-crypto swap as a taxable event, meaning every single line item requires precise date, time, and cost-basis tracking. Relying on memory or rough estimates invites audits and penalties.

To build a defensible tax record, you need a systematic approach to data collection. This process ensures you capture every trade, transfer, and staking reward before the tax year closes. Follow this three-step workflow to gather and verify your transaction data.

Most major exchanges, including Coinbase and Binance, allow you to export your complete trade history. Navigate to the reporting or history section and select the CSV or JSON format. Ensure you download data for the entire tax year, starting from January 1st. This raw file is your primary source of truth for trades executed on that platform. Keep these files in a secure, backed-up folder, as exchange data can sometimes be purged or altered after the fact.

Centralized exchange exports do not capture activity on self-custody wallets like MetaMask, Ledger, or Trust Wallet, nor do they cover decentralized exchange (DEX) swaps. Use blockchain explorers like Etherscan or Solscan to export your transaction history, or use wallet software that generates CSV reports. For DeFi users, this step is critical because every swap, liquidity provision, and yield farming interaction is a taxable event. Missing these logs creates gaps in your cost basis calculations.

Combine all exported CSVs into a single master dataset. Look for duplicates, missing dates, or incorrect asset symbols. Cross-reference your total trade count against your exchange statements to ensure nothing was left out. If you use a crypto tax software, import these raw files into the platform to automate the calculation of capital gains and losses. This aggregation step transforms scattered data into a structured record that you can review before filing.

Choose the right cost basis method

Your choice of cost basis method dictates which coins are "sold" first when you trade, swap, or spend crypto. This selection directly impacts your taxable gains or losses, especially in volatile markets where entry prices vary significantly. The IRS recognizes two primary methods: First-In, First-Out (FIFO) and Specific Identification (Specific ID).

FIFO: The Default Setting

FIFO assumes you sell the oldest assets first. If you bought Bitcoin in 2019 and again in 2021, selling a portion triggers a sale of the 2019 coins first. In a bull market, this often results in higher capital gains because older coins typically have lower cost bases. FIFO is simple and requires minimal record-keeping, but it may not be the most tax-efficient strategy for active traders looking to manage their tax liability.

Specific ID: The Active Trader’s Choice

Specific Identification allows you to choose exactly which units of crypto you are selling. If you bought 1 BTC at $20,000 and another at $50,000, you can sell the $50,000 coin to realize a smaller gain (or a loss) when selling at $60,000. This method offers greater tax control but requires meticulous record-keeping. You must track each specific unit’s acquisition date, price, and fees. The IRS requires that you identify the specific coins sold at the time of the transaction and report this on your tax return.

Comparison: FIFO vs. Specific ID

| Feature | FIFO | Specific ID |

|---|---|---|

| Tax Efficiency | Often higher gains in bull markets | Can minimize gains or harvest losses |

| Record Keeping | Simple; chronological order | Complex; requires unit-level tracking |

| IRS Compliance | Default method; easy to report | Requires explicit identification per trade |

| Best For | Passive investors or low-volume traders | Active traders managing tax liability |

Choosing the right method depends on your trading volume and tax goals. If you trade frequently, Specific ID can save you money, but it demands rigorous documentation. Always consult a tax professional to ensure compliance with current IRS guidelines.

Apply Section 475 mark-to-market

Mark-to-market (MTM) under Section 475 is the most powerful tax strategy for high-volume crypto traders. It treats your crypto assets as business inventory rather than capital assets. This election fundamentally changes how gains and losses are calculated, often saving traders thousands of dollars by eliminating the wash sale rule and allowing unlimited ordinary loss deductions against ordinary income.

How Section 475 Works for Crypto

Under standard capital gains rules, crypto is a "capital asset." If you sell a coin at a loss and buy it back within 30 days, the IRS considers it a wash sale, disallowing the loss. Section 475 changes this. By electing MTM, you agree to treat all your crypto holdings as if they were sold at fair market value on the last day of the tax year. This is called a "deemed sale."

Because your crypto is now classified as inventory, the wash sale rule no longer applies. You can buy and sell the same token repeatedly without losing your loss deductions. Also, MTM losses are treated as ordinary losses, not capital losses. This means you can deduct them against other income, such as wages or business revenue, without the $3,000 annual cap that limits capital loss deductions.

The Election Deadline

To use Section 475, you must file Form 3115 with the IRS. The deadline is strict: you must file this form by the 15th day of the fourth month of the tax year (typically April 15th) for that year. If you miss this window, you cannot apply the election retroactively. For a crypto trader, timing is everything; a late election can result in significant tax liabilities for the entire year.

Disclaimer: This information is for educational purposes only and does not constitute financial or tax advice. Tax laws are complex and subject to change. Consult a qualified tax professional or CPA to determine if Section 475 is appropriate for your specific trading activity.

Eligibility Requirements

Not every trader qualifies. The IRS requires that your trading activity is substantial, frequent, and continuous. While there is no specific minimum number of trades, courts have generally looked for traders who generate the majority of their income from trading rather than investment. If your primary goal is long-term appreciation, you likely do not qualify. If you are day-trading or swing-trading with high volume, Section 475 may be the right path.

Steps to Elect

- Review your trading volume: Ensure your activity meets the "substantial" threshold. Keep detailed records of all trades.

- Prepare Form 3115: Complete Form 3115, Application for Change in Accounting Method. File it with your federal tax return for the year you want the election to take effect.

- Attach a statement: Include a statement with your tax return indicating your intent to elect Section 475(e) for crypto assets.

- Consult a professional: Given the complexity, have a CPA verify your eligibility and filing to avoid IRS penalties.

Review tools for tax compliance

Active trading volume creates a data mountain that manual spreadsheets can’t handle. You need dedicated crypto tax software to aggregate transactions from wallets and exchanges, then map them to IRS reporting requirements. These platforms automate the heavy lifting, turning thousands of rows of trade history into clean Schedule D and Form 8949 entries.

When selecting software, prioritize tools that support high-frequency trading formats like CSV imports from major exchanges (Binance, Coinbase, Kraken) and DeFi protocols. Look for features like FIFO (First-In, First-Out) or HIFO (Highest-In, First-Out) lot matching, which directly impact your taxable gains. Avoid generic accounting software unless it has specific crypto plugins, as they often miss complex DeFi interactions.

Education is equally critical. The IRS treats crypto as property, meaning every swap, trade, or even spending event is a taxable occurrence. Use resources like the official IRS Notice 2014-21 and specialized guides from reputable financial educators to understand how your specific trading strategy fits into the broader tax code. Ignorance of the rules isn’t a defense, so verify your software’s output against official guidance.

For those who prefer structured learning, platforms like AvaAcademy offer free courses on cryptocurrency trading that often include modules on tax implications. These resources help bridge the gap between technical trading skills and financial compliance, ensuring you’re not just profitable, but also compliant.

As an Amazon Associate, we may earn from qualifying purchases.

Finalize your tax return

Filing your crypto taxes is the final step in a process that demands precision. For active traders, this isn't just about entering a few numbers; it's about accurately categorizing high-volume transactions across Form 8949 and potentially Schedule C if you are treated as a dealer. Missteps here can trigger audits or unnecessary penalties, so treating the filing phase with the same rigor as your trading strategy is essential.

1. Reconcile your transaction data

Before opening your tax software, ensure every trade from every exchange and wallet is accounted for. Import your CSV files and cross-reference them against your internal records. Look for missing staking rewards, airdrops, or DeFi interactions that automated importers often miss. If you are a high-frequency trader, verify that your cost basis method (FIFO, LIFO, or Specific ID) is applied consistently across all entries.

2. Complete Form 8949

Form 8949 is where you report sales, exchanges, and disposals of virtual currency. Each transaction gets its own line item, detailing the date acquired, date disposed, proceeds, cost basis, and gain or loss. For active traders, this form can become lengthy. If you have thousands of transactions, consider using a qualified tax professional or specialized software that can aggregate these entries efficiently while maintaining IRS compliance. IRS Publication 544 provides the official instructions for reporting property, including digital assets.

3. Determine Schedule C eligibility

Most individual investors report crypto gains on Schedule D, which flows from Form 8949. However, if you are an active trader acting as a dealer—buying and selling with the primary purpose of profiting from short-term market movements—you may need to report on Schedule C. This changes your tax treatment significantly, allowing for ordinary income rates and potentially deducting business expenses. The distinction between an investor and a dealer is nuanced; consult the IRS guidance on virtual currencies to determine your status.

4. Review and file

Once your forms are populated, review the summary for accuracy. Check for any unclaimed deductions or errors in cost basis calculations. If you owe taxes, ensure you have funds set aside to cover the liability. File your return by the deadline, April 15th, or request an extension if necessary. Keeping detailed records of your filing and supporting documents is crucial for future audits.

-

Verify all exchange CSVs are imported and reconciled

-

Confirm cost basis method is consistent across all transactions

-

Review Form 8949 for accuracy and completeness

-

Determine if Schedule C is required based on trading activity

-

Ensure tax liability funds are set aside for payment

No comments yet. Be the first to share your thoughts!